- Senator Elizabeth Warren’s bill on anti-money laundering in crypto is gaining momentum with new sponsors.

- It includes provisions that could force crypto firms to collect data on customers.

- Legal scholars doubt the bill will pass into law.

- But aspects of it may slip into other laws, and it's a sign politicians are seizing on sentiment.

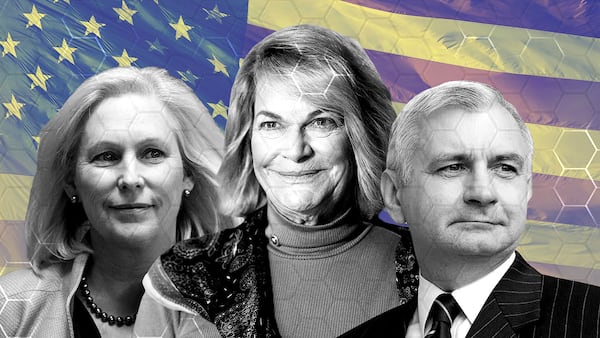

Senator Elizabeth Warren this week gained five new backers for a bill that would clamp down on cryptocurrencies used in money laundering and terrorism financing.

While experts cast doubt on the likelihood of it ever making it off the Congress floor, it’s a major warning sign.

“This better be a wake-up call for the industry to come forward with serious proposals on how to counter terrorist financing and anti-money laundering in crypto,” Rebecca Rettig, chief legal and policy officer at Polygon Labs, told DL News. “There is clearly some steam gaining behind the movement to find some solution.”

Critics fear the Anti-Money Laundering Act, introduced in 2022, would turn tech actors, such as software developers, into financial intermediaries forced to collect and report user data that could cause a security threat.

A policy insider told DL News that elements of the act could work their way into other rules.

Even as some have downplayed Warren’s weak track record in passing bills into law, it is not uncommon for lawmakers to break up legislative texts and stick them on different bills.

While this may not materialise in 2024 when other policies take priority — and the presidential election may grind the legislative process to a halt — pieces of the bill may resurface in 2025, the insider said.

Another worry: The “bill would do nothing to stop bad actors from abusing this technology,” Kristin Smith, CEO of the Blockchain Association lobbying group, told DL News.

Rather, it could chase crypto activity offshore, she said.

Lawmakers have seized on reports on the use of crypto in financing Hamas and other illicit groups to add urgency to this and other anti-crypto legislation. And public perception of crypto hasn’t been helped by headlines about the collapse of FTX and billions in fines for Binance.

Breathe easy

Critics can breathe easy, for now.

“I don’t think this bill is going anywhere,” Austin Campbell, managing partner of Zero Knowledge Consulting and adjunct professor at Columbia business school, told DL News.

“If somehow they managed to get a critical mass of the Senate, which I think is unlikely, I don’t think it has a future in the House,” said Campbell.

For a bill to become law, it needs support from both Republican and Democrat parties, as well as from both the Senate and the House of Representatives in Congress.

Gautam Chhugani, senior analyst on digital assets at Bernstein Research, echoed that view. He is “not worried” and said the bill is “another impractical anti-crypto posturing, likely to meet a dead end.”

Warren’s anti-money laundering bill gains sponsors

Their comments came as five more Democrat senators signed on to the Anti-Money Laundering Act, Warren said on Monday. That adds up to 21 senators backing the bill, which calls for a crackdown on crypto service providers and more Treasury oversight.

“Our bipartisan bill is the toughest proposal on the table cracking down on crypto’s illicit use and giving regulators more tools in their toolbox,” said Warren in a statement.

Senator Roger Marshall, a Republican from Kansas is a cosponsor of the bill, providing bipartisan legitimacy to the bill.

The US Treasury “is making clear that we need new laws to crack down on crypto” and its uses in illicit financing, Warren added.

Two weeks ago, the Treasury Department requested that Congress grants it additional powers to seize crypto assets used in illicit financing, DL News previously reported. This was met with concern in the industry.

Since reports of crypto used in financing organisations such as Hamas following the October 7 attack, lawmakers and regulators turned their attention to how crypto is used to finance terrorism.

The industry has since endeavoured to demonstrate how blockchain as a technology can help authorities track down illegal actors, and rejected findings of a widely criticised article by The Wall Street Journal.

A big worry: the merging of technology service providers, like digital wallet software, crypto miners and validators, would be implicated into financial services rules.

Campbell argues the bill could create “absolutely massive security problems,” since it would require “people who have no regulatory framework and no expertise to collect everybody’s private personal data.”

His criticism is that the provisions would target the technology rather than the criminal actions.

Inbar Preiss is a Brussels-based correspondent who covers crypto regulatory policy. Have a tip? Contact the author at inbar@dlnews.com.